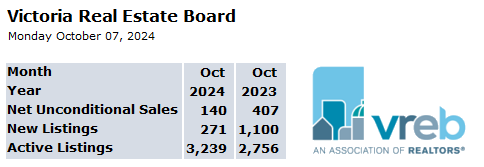

A total of 367 properties sold in the Victoria Real Estate Board region this December, 12.8 per cent fewer than the 421 properties sold in December 2024 and 18.6 per cent fewer than in November 2025. Sales of condominiums were down 21.5 per cent from December 2024 with 106 units sold. Sales of single family homes decreased by 2.6 per cent from December 2024 with 186 sold.

There were 6,918 sales over the course of 2025, a 0.36 per cent increase from the 6,893 sales in 2024.

“2025 was another consistent year for local real estate,” said 2026 Victoria Real Estate Board Chair Fergus Kyne. “Despite global economic uncertainty, property sales in the Victoria market were steady and pricing remained relatively balanced. One of the most significant factors in 2025 was the amount of available inventory. We saw the second highest number on record of new listings enter the market. The ample inventory was good news for sellers and for the stability of our market. Buyers had more choice and time to make decisions, while sellers benefitted from clearer expectations around pricing and timelines.”

There were 2,544 active listings for sale on the Victoria Real Estate Board Multiple Listing Service® at the end of December 2025, a decrease of 19.3 per cent compared to the previous month of November but an 11.1 per cent increase from the 2,290 active listings for sale at the end of December 2024.

The Multiple Listing Service® Home Price Index benchmark value for a single family home in the Victoria Core in December 2024 was $1,316,700. The benchmark value for the same home in December 2025 decreased by 4.7 per cent to $1,255,000, down 1.7 per cent from November’s value of $1,276,700. The MLS® HPI benchmark value for a condominium in the Victoria Core area in December 2024 was $546,100 while the benchmark value for the same condominium in December 2025 increased by 0.7 per cent to $549,900, a decrease of 0.6 per cent from the November value of $533,100.

Victoria BC Market Stats Update December 2025